At a time when the demand for advice by Australians has never been greater, Sarah Abood (FAAA) and Patrick Hartney (AFCA) discuss how the advice environment can be improved and what to expect from ASIC’s review of the managed accounts sector.

At a time when the demand by consumers for quality advice continues to increase sharply, it’s hardly surprising that the burden of regulation and government red tape has seen the number of advisers in Australia steadily decrease — from an industry high of 28,914 to today’s number of 15,127 (as at 12/3/26).

It’s a drop in numbers that concerns Sarah Abood — CEO of the Financial Advice Association Australia (FAAA) — who acknowledges the number of challenges facing the advice profession, with five being particularly challenging for advisers:

1. Government red tape;

2. Input costs — including some costs that are unique to the sector (ASIC and the Compensation Scheme of Last Resort levies), as well as other costs which are economy-wide;

3. Staffing — finding, recruiting and keeping quality people, and the costs involved in doing so;

4. Technology — selecting and managing the ‘tech stack’, cybersecurity, and grappling with the rise and use of artificial intelligence; and

5. Defending the profession — from multiple areas, including consumers, regulators, and Government.

By Jayson Forrest

Patrick Hartney

Senior Ombudsman

Australian Financial Complaints Authority

Sarah Abood

Chief Executive Officer

Financial Advice Association Australia

Continued.....

Yet, despite these challenges, in a session on ‘The 2026 challenges for advisers’ at the IMAP Portfolio Management Conference in Sydney, Sarah says the advice sector remains healthy, with approximately 58-62 per cent of advice practices using managed accounts, with more intending to do so in the future.

However, she recognises that the strong growth of managed accounts has attracted the attention of ASIC, which seeks to better understand potential risks to retail investors using this structure. The regulator is already in the process of examining the managed accounts sector (specifically SMAs), where its primary focus in 2025-26 is to conduct surveillance on licensees and advisers to ensure compliance, proper governance, and good consumer outcomes.

“This discovery process that ASIC is currently undertaking is broadly across managed accounts. ASIC is looking at the advice (licensees and advisers) and provider side of managed accounts, as well as consumer outcomes using this structure,” says Sarah

We don’t know whether ASIC’s review of the managed accounts sector is ‘risk-weighted’. However, when the report is finally released, it will be important to know whether this review was targeted to areas that ASIC believes are high risk or whether it’s an impartial inquiry across the whole sector. At the moment, we just don’t know

Risk-weighted or not

Sarah is unsure whether ASIC’s review of managed accounts is ‘risk-weighted’. Occasionally, ASIC conducts ‘risk-weighted’ reviews into sectors where it knows there are existing problems. As an example, Sarah refers to the recent report on self-managed super funds (SMSFs), which was a ‘risk-weighted’ exercise.

“We don’t know whether ASIC’s review of the managed accounts sector is ‘risk-weighted’. However, when the report is finally released, it will be important to know whether this review was targeted to areas that ASIC believes are high risk or whether it’s an impartial inquiry across the whole sector. At the moment, we just don’t know.”

In terms of the review, Sarah believes ASIC is focusing its attention on the following six areas:

- Incentives, including sales and revenue targets;

- Management of conflicts;

- Governance frameworks;

- Conduct obligations;

- Consumer outcomes; and

- Transparency — particularly around portfolio holdings and fees.

“Of these six areas, we believe incentives and management of conflicts are the two main areas in ASIC’s focus,” says Sarah. “We’re hearing ASIC is specifically looking at incentives, including inappropriate payments, like sales and revenue targets. It’s looking at incentives that may already be banned or are inappropriate in this space. And management of conflicts is another key focus area for ASIC, with the regulator recently re-releasing RG 181 (AFS licensing: Managing conflicts of interest).”

Other areas that are likely to be ‘red flags’ for ASIC include: no independent oversight of the portfolio; use of many related party products; fees that are high, layered, and/or not transparent; lack of transparency with portfolio holdings; and persistent underperformance of the portfolio with no action taken

Satisfying the Best Interest Duty

Although the types of questions ASIC is asking as part of the review are quite broad, Sarah believes it’s essential that licensees and advisers are able to satisfy compliance with the Best Interest Duty. This includes:

- Evidence of consideration of individual client needs and goals (risk profile, tax issues, liquidity needs, time horizon, income needed, and investment preferences, like ESG);

- No ‘cookie cutter’ advice (like re-wording a strategy in an SOA as a client goal);

- Due diligence and ongoing monitoring of the portfolio; and

- No conflicted remuneration or inappropriate incentives (which have been illegal since July 2013).

“Other areas that are likely to be ‘red flags’ for ASIC include: no independent oversight of the portfolio; use of many related party products; fees that are high, layered, and/or not transparent; lack of transparency with portfolio holdings; and persistent underperformance of the portfolio with no action taken.”

Sarah confirms the ASIC review is well underway, with the regulator expected to report back to the industry this calendar year.

<sub>Managed account complaints

With managed accounts firmly in ASIC’s spotlight, this structure only represents a small number of complaints lodged to the Australian Financial Complaints Authority (AFCA) — a free, independent and impartial service to assist individuals and small businesses to resolve complaints about financial products and services.

In a session titled, ‘When things go wrong’ at the 2026 IMAP Portfolio Management Conference in Melbourne, Patrick Hartney — Senior Ombudsman at AFCA — says of the 57,147 complaints received by AFCA in the past six month period (1 July 2025 to 31 December 2025), there were 3,165 complaints received in relation to investments and advice, primarily due to the Shield and First Guardian collapse, which impacted many consumers.

However, while AFCA does not have specific statistics on SMAs, it has been tracking MDAs for a number of years. For the MDA sector, of the total number of complaints received by AFCA over this same period, only 10 complaints were in relation to MDAs (where the MDA was listed as ‘the product’).

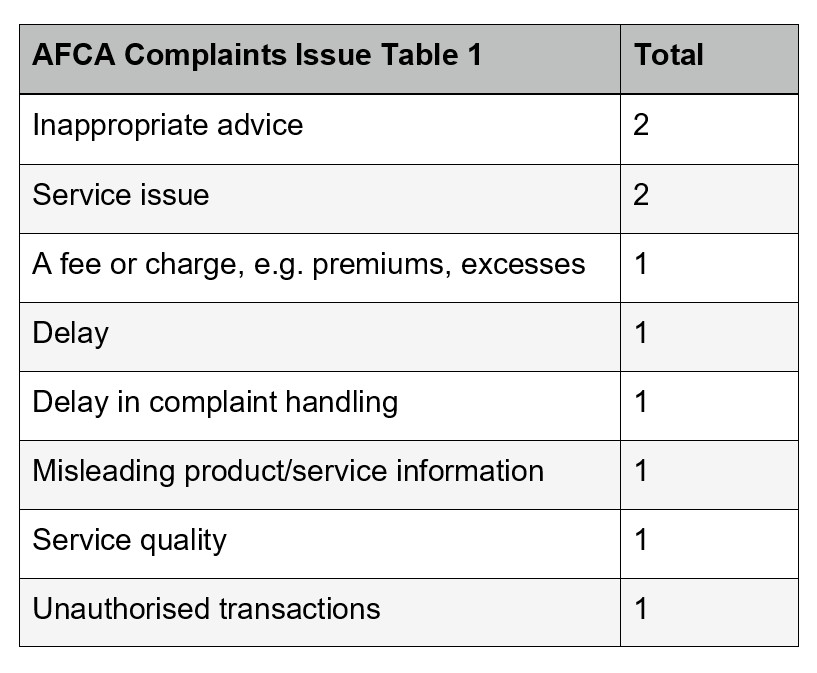

These 10 complaints included:

Five of these complaints were closed during this six month period (1 July 2025 to 31 December 2025), with the average time to close a complaint being 54 days. When explaining these 10 complaints, Patrick says it’s not uncommon for clients to not be completely aware of what product they have or what product they are actually complaining about.

“For example, some clients might say they are complaining about their shares, when in fact, they are actually complaining about the advice they’re receiving on the MDA,” says Patrick. “From time to time, we also receive complaints around discretionary trading when both the structure and licence weren’t in place. This is where AFCA’s systemic issues function comes into play, where we have an obligation to report serious misconduct or systemic breaches to the regulators.”

Patrick adds that with the few MDA complaints received to date, they do tend to be of a higher value, where one party might be looking at, say, $500,000 for a claimed loss, while the other party is looking at $0. This does make it more difficult to find the middle ground when resolving complaints.

From time to time, we also receive complaints around discretionary trading when both the structure and licence weren’t in place. This is where AFCA’s systemic issues function comes into play, where we have an obligation to report serious misconduct or systemic breaches to the regulators

10 tips to avoid complaints

To assist advisers avoid MDA complaints, Patrick offers the following 10 tips:

1. Take detailed file notes.

2. Clearly explain the scope of advice. It is extremely important to ensure the client actually understands the scope of advice.

3. Have a clear understanding of the client’s goals and objectives, and summarise them. For example, avoid goals and objectives that are broad and hard to measure, like ‘wealth creation’ or ‘capital security’, which can be difficult to justify in an advice situation. Instead, be specific, like: ‘To retire at age 65 on an income of $50,000 per annum.’ And remember to articulate how the recommended strategy will achieve the client’s goals and objectives.

4. Understand and explain the products being recommended. As products are getting increasingly more complex, advisers need to avoid jargon and technical descriptions, and instead, explain products to clients simply. This helps to ensure clients understand what they are investing in.

5. Ensure you have good reasons to recommend a switch. Advisers need compelling reasons to recommend a change of products and/or investments.

6. Turn clients away if necessary. This is particularly important if an adviser or advice business doesn’t offer the product or have the requisite expertise with a product or service, like an MDA. Also, carefully consider how to proceed if clients are seeking a return that does not match their risk profile.

7. Use risk profiling tools carefully. This includes: considering inconsistencies in answers provided; considering the client as a whole; and not to amend the risk profile lightly.

8. Manage conflicts of interest adequately. This means prioritising the client’s interests ahead of an adviser’s interests.

9. Carefully document if a client wants to act against your advice. This includes whether you are endorsing the advice, or whether you are providing an execution-only service.

10. Make sure the client provides informed consent to the advice. Ensure you sign off on authorities to proceed with the advice, and you have a clearly documented paper trail to proceed with the advice.

At AFCA, we act as a circuit breaker and help build trust between affected parties, while providing an independent view based on fairness. We always aim to be flexible and adaptable to meet the needs of affected parties

The role of AFCA

Ask Patrick and he will tell you AFCA is successfully helping to improve the advice environment by: resolving complaints, identifying systemic issues and working with financial firms to resolve them, and supporting regulators by reporting certain matters to them.

“AFCA can play an important role in the resolution of financial complaints,” he says. “It’s in everyone’s interest to have matters resolved quickly. So, in a three-way discussion — between the complainant, AFCA, and the respondent — we can help to get all involved parties talking.

“At AFCA, we act as a circuit breaker and help build trust between affected parties, while providing an independent view based on fairness. We always aim to be flexible and adaptable to meet the needs of affected parties.”

About

Sarah Abood is CEO of the Financial Advice Association Australia (FAAA), and

Patrick Hartney is Senior Ombudsman at the Australian Financial Complaints Authority (AFCA).

They spoke on the topics ‘The 2026 challenges for advisers’ and ‘When things go wrong’ at the 2026 IMAP Portfolio Management Conference in Sydney and Melbourne.